Australia’s nationwide hotel room inventory has soared past the 300,000 hotel room mark, according to new data on November openings from STR, solidifying the country’s strong appeal among global investors and developers.

The STR data revealed the country now features 5,600 commercial hotels and 300,229 rooms, based on the company’s pre-defined qualification data. The data company counts a hotel as generating revenue on a nightly per-room basis, operating 10 rooms or more and being available to the public (excluding membership or affiliation properties).

With more than 26,000 rooms added to the marketplace since 2016, the milestone sees Australia ranked fourth in the Asia-Pacific and 12th in the world for total room count. The figures exclude more than 5,000 rooms which closed in the same period for conversion into other accommodation types.

Australia’s ten major cities and regions (eight state and territory capitals plus Cairns and Gold Coast) make up 57.1% of the country’s hotel inventory, with the majority of rooms (47.8%) sitting in the Upscale and Midscale price categories.

STR Regional Manager, Asia-Pacific, Matthew Burke, said the improved investment reflected the country’s strong hotel performance, especially in major markets.

“As a whole, Australia’s occupancy has been at or near 75% for each of the last five years, and average daily rate has consistently ranged around 185 Australian dollars.”

Sydney led the way for hotel room inventory in Australia with 43,841 rooms. On a branded basis, Accor is the dominant leader for market share, operating 32.1% of all qualifying rooms. The Ascott Limited was a distant second with 7.6%.

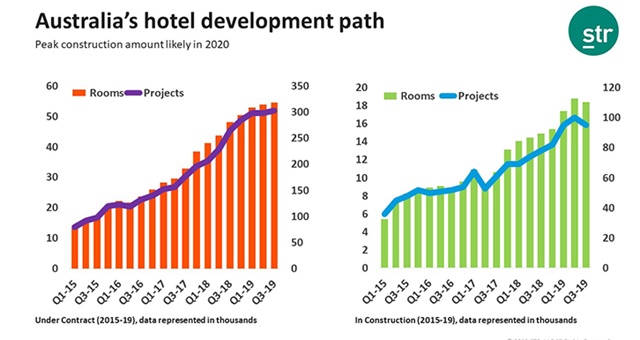

After several years nudging capacity constraints, new hotel supply has dominated 2019 and put pressure on RevPAR and Average Daily Rate, despite occupancy remaining strong and limiting the damage somewhat. Australia currently has 94 hotel projects in the pipeline, comprising 18,294 rooms, with another 216 projects still in planning phases.

The STR data showed Adelaide, Hobart and Melbourne would see the largest increase in room capacity as development continues to escalate ahead of an expected peak next year.

“Moving forward we anticipate demand growth in almost all markets, but with sustained supply increases, we’re still forecasting occupancy declines in the short term,” Burke added.

“Room rates will of course be weighed by the additional competition in the market, but that is not likely to become a long-term trend as many markets trade at high absolute occupancy levels with the ability to absorb new supply.”